When Spectrum Turns Into Venture Capital

EchoStar, SpaceX, xAI, Grok and the Cost of Blurred Balance Sheets

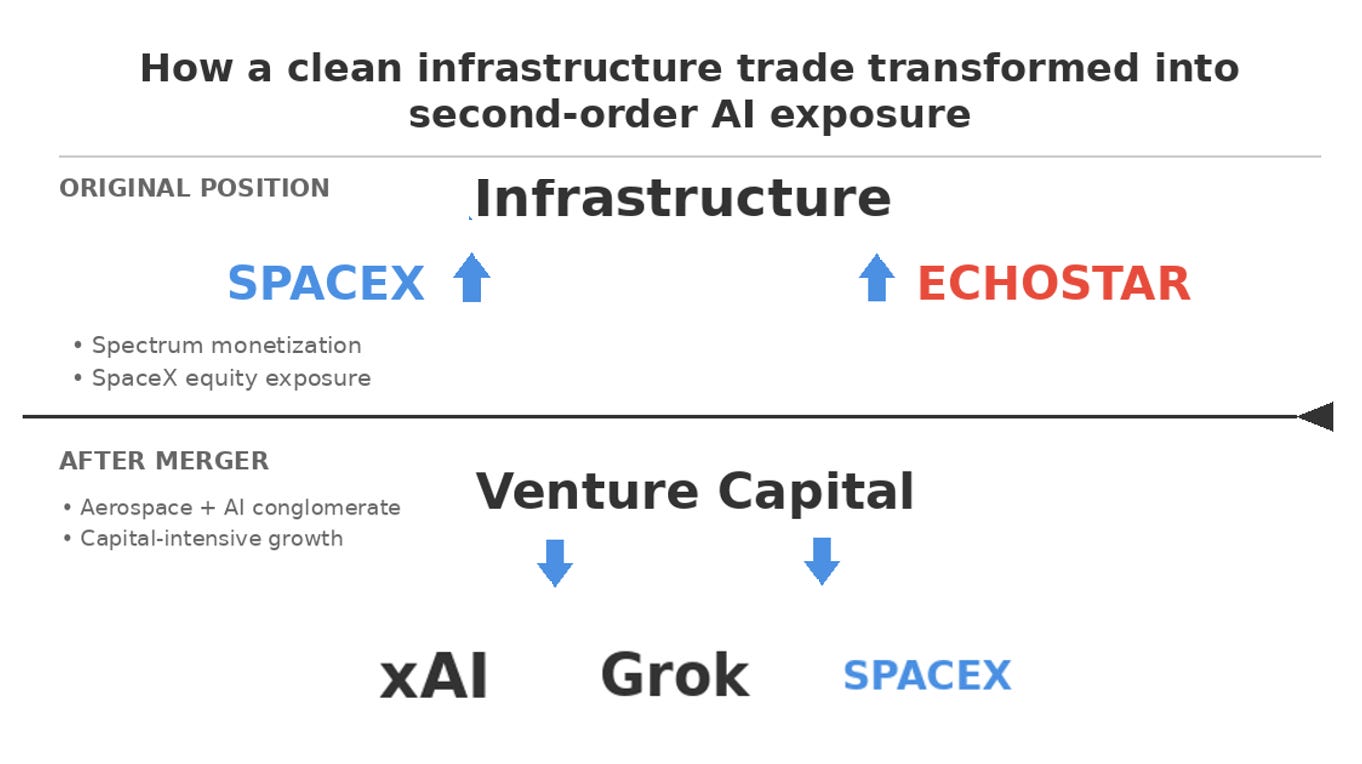

For a brief moment, EchoStar appeared to have executed one of the cleanest strategic pivots in modern telecom history.

A deeply levered, spectrum-heavy company monetized scarce regulatory assets at scale, secured billions in liquidity, stabilized its balance sheet, and converted stranded licenses into long-term optionality. Markets rewarded the clarity. EchoStar shares more than tripled.

Then the story changed

Not because the spectrum transactions unraveled. Not because SpaceX faltered operationally. But because SpaceX merged with xAI, quietly transforming EchoStar’s upside from a clean infrastructure exposure into a second-order venture capital bet.

The recent market pullback reflects that realization.

The Original Trade: Spectrum as Balance-Sheet Repair

EchoStar’s transactions with SpaceX were initially elegant in both form and intent. The company agreed to sell AWS-4 and H-block licenses for approximately $17 billion in cash, while transferring unpaired AWS-3 licenses in exchange for roughly $11 billion in SpaceX equity. In aggregate, EchoStar emerged with an estimated 3% ownership stake in SpaceX.

This was not speculative behavior. It was necessity-driven capital discipline. Cash proceeds repaired the balance sheet and reduced existential risk. Equity participation provided upside without immediate dilution.

The Inflection Point: SpaceX Merges With xAI

The merger fundamentally altered how SpaceX equity must be valued—and, by extension, how EchoStar should be priced.

Before the merger, SpaceX could plausibly be evaluated on launch dominance, Starlink growth, and improving unit economics. After the merger, SpaceX equity absorbs AI-scale cash burn, competitive uncertainty, and founder-driven capital allocation without explicit ring-fencing.

Why This Matters More for EchoStar Than SpaceX

EchoStar does not control SpaceX governance. It owns marked private equity whose value now depends on IPO timing, conglomerate discounts, AI funding needs, and liquidity windows.

This shifts EchoStar from a telecom monetization story into a holding company proxy for a merged aerospace-AI venture an uncomfortable position for public markets.

Bottom Line

EchoStar executed one of the most consequential spectrum monetizations in telecom history. But by accepting equity in a company that later merged with a capital-intensive AI venture, it unintentionally shifted shareholders into a different risk universe.

Valuation discipline matters most at the boundary between infrastructure and experimentation. EchoStar now sits precisely on that boundary.

Our Full EchoStar–SpaceX Valuation Risk Report Includes:

Scenario-based valuation bands for EchoStar under multiple SpaceX/xAI capital-allocation outcomes

Governance and dilution risk mapping tied to private-market structure and IPO mechanics

Liquidity and monetization pathway analysis for EchoStar’s SpaceX equity stake

Conglomerate-discount modeling and historical precedent comparisons

Early-warning indicators that signal valuation inflection points before public repricing

An integrated framework linking spectrum monetization, balance-sheet repair, and venture-risk transmission

To purchase a copy of our detailed EchoStar–SpaceX Valuation Risk Report, click the button below.