The Capital Consequences of Over-Fragmented Network Markets

Generally, competition is commonly assumed to improve aggregate adoption and economic scale.

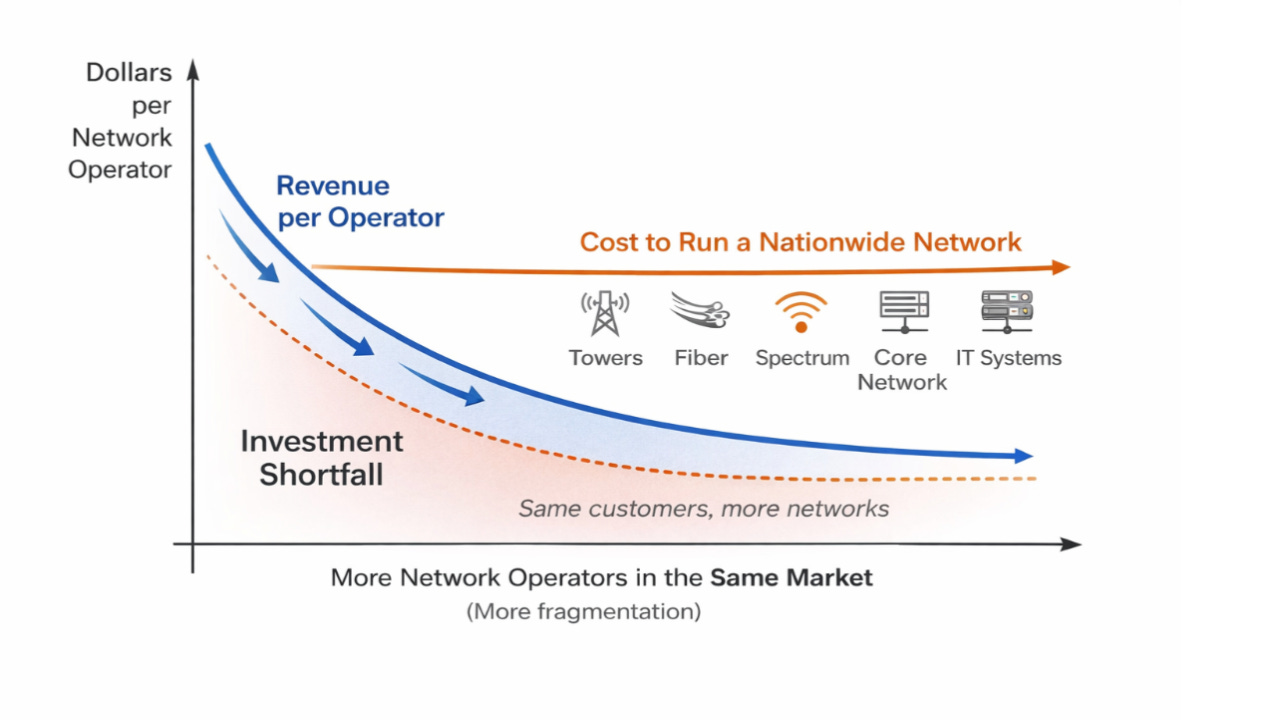

In capital-intensive network industries, excessive fragmentation often produces the opposite effect.

Fiber overbuild, wireless expansion, densification efforts, nationwide coverage, core transport network and infrastructure platforms are dominated by fixed and sunk costs. These costs do not scale downward as pricing pressure increases. When too many operators pursue the same demand pool, revenues fragment rapidly while the cost base remains largely intact.

Pricing adjusts immediately. Capital investment does not.

Over time, this mismatch constrains reinvestment, delays modernization, and erodes network quality—not suddenly, but incrementally. The resulting underperformance is frequently attributed to management execution or regulatory friction rather than to structural economics.

Markets with fewer facilities-based operators consistently demonstrate higher investment per subscriber and faster technology deployment. The distinction is not strategic philosophy or operational virtue. It is capital capacity.

Fragmentation does not discipline inefficiency.

It systematically starves investment.

Importantly, fragmentation is not inherently destructive. It becomes damaging when it occurs at the facilities layer of capital-intensive networks.

Competition can be highly effective when applied above the infrastructure stack rather than within it. Service-level competition—pricing, bundling, customer experience, vertical specialization—can flourish atop a consolidated physical network without impairing investment incentives.

Infrastructure competition duplicates fixed costs.

Service competition exploits them.

Wholesale access models, MVNOs, open-access fiber, neutral-host networks, and shared RAN architectures preserve scale economics while enabling meaningful competition. In these structures, price pressure disciplines margins without hollowing out capital formation.

The failure is not competition itself, but misalignment of competition with cost structure.

Investor Takeaway

In network industries, market structure precedes performance. Fragmented revenue bases interacting with non-scalable cost structures produce predictable capital stress long before it appears in reported KPIs.

Early warning signs are structural, not operational: declining investment per subscriber, deferred modernization cycles, rising maintenance intensity, and increasing reliance on financial engineering to sustain returns. These conditions are often misread as execution issues rather than economic inevitabilities.

Conversely, markets with fewer facilities-based operators sustain higher capital intensity, faster technology deployment, and greater resilience across cycles. The premium these assets command reflects durable capital capacity, not scarcity alone.

Capital does not fail randomly in network markets.

It fails where structure makes reinvestment mathematically optional.

About Bill Stueber

Bill Stueber is a telecom industry veteran focused on the structural economics of networks, capital allocation, and valuation. His work examines why traditional growth, scale, and pricing assumptions frequently fail in telecommunications—and how those failures create persistent mispricing across assets, technologies, and cycles.

He has spent decades operating, financing, and analyzing telecom infrastructure, with experience spanning wireless, fiber, spectrum, and network economics. His current work centers on translating complex technical and regulatory dynamics into frameworks investors can actually underwrite.

Bill writes independently and engages selectively on questions of valuation, diligence, and structural risk.

#Telecom

#InfrastructureInvesting

#TMT

#CapitalMarkets

#NetworkEconomics

#Valuation