The 4th Layer of Connectivity

Wireless is quietly adding an orbital overlay — turning coverage from a footprint problem into a continuity product.

Wireless is quietly adding an orbital overlay — turning coverage from a footprint problem into a continuity product.

The investor-level question is no longer “Is satellite real?” It’s: who captures the economics when ‘no signal’ stops being acceptable?

What’s Changing

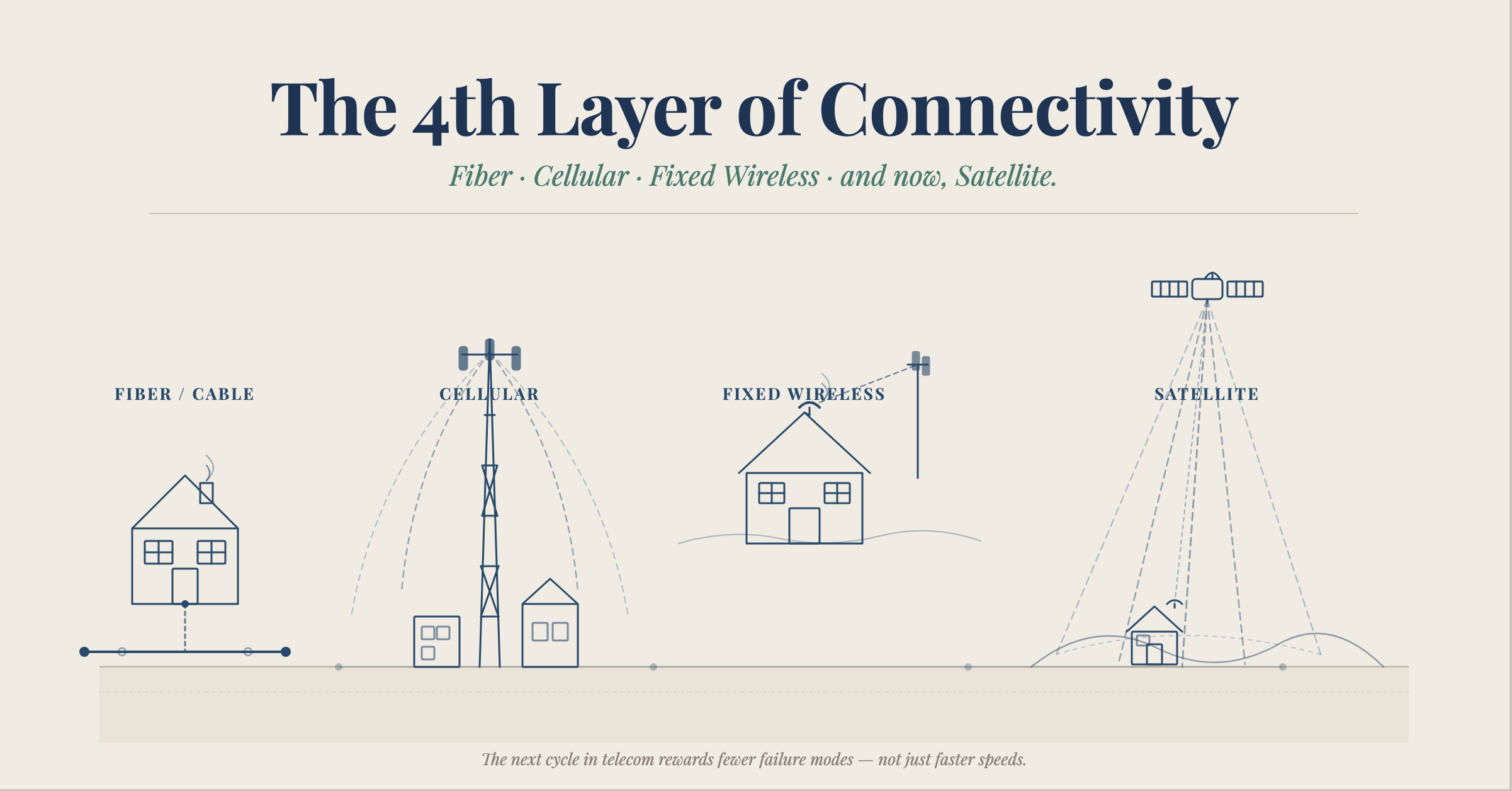

For decades, mobile networks were constrained by geography: towers and terrain determined where you could connect. Now carriers are positioning satellites as a complementary layer for those rare but high-stakes moments when terrestrial coverage falls short — wilderness, highways, lakes, rural edges, disaster zones.

Evidence the Industry is Past the ‘Science Project’ Phase

AT&T signed a definitive commercial agreement with AST SpaceMobile to deliver space-based broadband direct to everyday cell phones, explicitly framing it as complementing and integrating with its existing mobile network.

Verizon and AST SpaceMobile demonstrated a live video call with one device connected via satellite and the other on Verizon’s terrestrial network — positioning satellite-to-device as an added reliability layer beyond tower reach.

T-Mobile is already marketing satellite-to-mobile as a consumer feature set, explicitly tying it to ending dead zones and extending messaging and select apps beyond tower coverage.

EchoStar’s combination with DISH was built around converged terrestrial and non-terrestrial connectivity, with an asset base structured to reduce near-term capex requirements.

Why This Hits Investors Where It Matters

1. Churn weapon, not just a feature. If “I can always get a message out” becomes an expectation, that’s sticky. Churn reduction can be more valuable than a modest ARPU add-on.

2. The definition of “best network” is changing. It stops being about speed tests in cities and becomes about fewer failure modes — connectivity that doesn’t disappear when it matters most.

3. Spectrum and network economics get a new dimension. An orbital layer changes the marginal economics of rural coverage. Depending on deal structure, it can reduce the need for certain ground up builds — or shift capex toward integration and capacity planning.

Where Each Ticker Fits

AT&T (T): Positioning satellite-to-device as a network extension via its AST partnership.

Verizon (VZ): Positioning satellite as an added reliability layer; active progress via satellite-to-device trials with AST.

T-Mobile (TMUS): Already moving the concept into consumer expectation and marketing, leading the continuity narrative.

AST SpaceMobile (ASTS): The direct-to-device enablement partner that carriers are commercializing against.

EchoStar (SATS): A converged satellite + terrestrial asset base thesis via the DISH combination, framed around global connectivity and capex/cash flow positioning.

The Questions I’d Demand Answers to Before Overweighting Any of Them

Economics: Wholesale input or retail differentiator?

Pricing model: Per-subscriber, per-MB, per-coverage-area, or revenue share?

Capability curve: Emergency texting only — or voice, data, and video at scale?

Capacity and congestion: What happens when millions try to use it simultaneously?

Regulatory and interference: How quickly do approvals and spectrum coordination move?

Bottom Line

This isn’t just a satellite story. It’s a network architecture story.

The next cycle in telecom will reward whoever can sell fewer failure modes — not just faster speeds. The orbital overlay is becoming the new expectation layer, and investors should underwrite it accordingly.

Bill Stueber is a 40-year telecom industry veteran focused on the structural economics of networks, capital allocation, and valuation. His work cuts through traditional assumptions around growth, scale, and pricing to determine what actually drives value as new technologies and competitive intensity reshape telecom economics. He engages selectively with investors to assess infrastructure asset values for acquisitions and existing portfolio companies through a structural risk and diligence lens. Bill is available for engagement through all major Expert networks