Telecom Infrastructure's Quiet Crisis

When Good Execution Isn't Enough

For the better part of a decade, telecom infrastructure investing benefited from a forgiving alignment: long-duration capital, stable demand growth, improving unit economics, and cheap leverage.

That alignment is breaking.

Not violently. Not all at once. But persistently enough that many assets will fail to earn the returns they were underwritten to deliver—even if they execute exactly as planned.

The problem is not poor management or bad forecasting. The problem is that the ROI window is shrinking, while most underwriting models still assume it is intact.

The Hidden Assumption No One States Explicitly

Every telecom infrastructure investment rests on a quiet premise:

The economic value created by this network will persist long enough, and at a high enough level, to recover capex and earn the projected return.

That premise used to be reasonable. It is becoming less so.

The issue is not whether demand for connectivity exists—it does. The issue is whether the value of that demand remains monetizable at the level and duration assumed.

This is a duration problem disguised as a growth problem.

Why the ROI Window Is Compressing

Three forces are converging—independently manageable, collectively destabilizing:

1. ARPU Is Behaving Like a Commodity, Not a Growth Asset

Most models still treat ARPU as stable to modestly rising, or declining slowly enough to be offset by scale.

But competitive reality is doing something different.

Across fiber, fixed wireless, and hybrid networks, price competition is intensifying, product differentiation is narrowing, and subsidies are pulling forward supply faster than demand quality improves.

The result is not collapse. It is compression—steady, rational, relentless.

When ARPU compresses faster than expected, the back half of the ROI window quietly disappears.

2. Capex Is Front-Loaded, Returns Are Not

Telecom infrastructure is inherently front-loaded: capital is deployed early, payback is long-dated, and returns depend on durability, not just uptake.

The economic half-life of the asset is shortening, even as the accounting life remains unchanged.

This worked when competitive intensity increased slowly, technology cycles were forgiving, and capital costs declined over time.

Today, technology substitution risk arrives sooner, competitive overbuilds occur faster, and capital costs are no longer declining.

That mismatch is fatal to long-duration return assumptions.

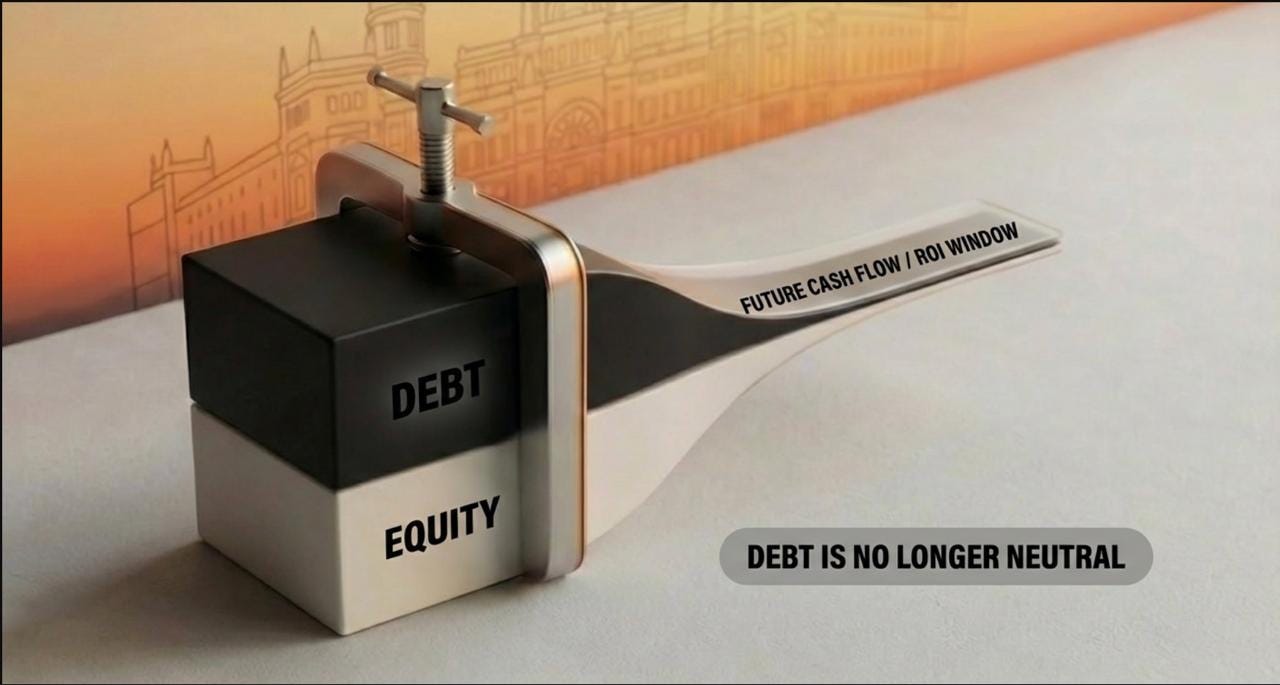

3. Debt Is No Longer a Neutral Amplifier

For years, leverage solved a lot of sins. It smoothed equity returns, rewarded early scale, and postponed hard questions.

Now debt is doing the opposite.

Refinancing risk, covenant sensitivity, and cost of capital are becoming binding constraints, not background variables. When debt tightens, equity upside caps sooner, strategic flexibility narrows, and duration mistakes surface early.

Debt is the first place the shrinking ROI window shows up—long before equity models admit it.

Why KPIs Are Lying (Without Intending To)

Most assets still look “fine” by traditional measures: subscriber growth, passings, take rates, near-term cash flow.

These KPIs are not wrong. They are incomplete.

They were designed for a world where duration was assumed, pricing power eroded slowly, and competitive structure evolved predictably.

In a world of faster substitution, subsidy-accelerated builds, and pricing convergence, KPIs lag economics.

By the time KPIs break, the ROI window is already closed.

This Is Not a Timing Call

This is not a claim that assets are suddenly worthless, that telecom infrastructure is broken, or that capital should flee the sector.

This is a claim that return expectations are misaligned with economic durability, duration risk is underpriced, and cross-capital-stack assumptions are inconsistent.

The danger is not immediate loss. The danger is structural underperformance that reveals itself too late to fix.

The Capital Stack Sees This Differently—And That Matters

Equity narratives can absorb optimism longer than debt reality can.

Credit feels the shrinking ROI window first: through refinancing friction, through tighter covenants, through reduced tolerance for volatility.

When debt becomes cautious, equity stories lose oxygen.

This is why recalibration must happen across debt and equity simultaneously, not sequentially.

What Sophisticated Capital Is Starting to Do Differently

The best allocators are not exiting en masse. They are quietly adjusting: shortening duration assumptions, stress-testing late-cycle cash flows, re-weighting exposure across capital structures, and treating policy and subsidy changes as economic accelerants, not stabilizers.

Most importantly, they are asking a harder question:

Not “Will this asset grow?” but “For how long will this asset earn what we think it will?”

That question changes everything.

The Real Risk

The real risk is not being wrong on growth.

The real risk is being right on execution, but wrong on durability.

That is how capital gets trapped—not through failure, but through slow erosion that never quite triggers alarm bells.

The ROI window doesn’t slam shut. It narrows—quietly—until returns fall short for reasons no single model line item can explain.

Final Thought

Telecom infrastructure is not becoming uninvestable. But it is becoming less forgiving.

Models that assume yesterday’s ROI window will persist are not aggressive—they are outdated.

The next cycle will not punish optimism. It will punish unexamined duration.

And by the time pricing reflects that reality, the opportunity to recalibrate will already be gone.

This is part of a series examining how structural shifts in telecom infrastructure are reshaping capital allocation before those changes appear in reported metrics. Subscribe to The Stueber Brief for analysis that catches inflection points while positioning flexibility still exists.